3月14日,朝鲜向日本海发射弹道导弹。同一周,卫星跟踪数据证实,大约 1,200 艘中国渔船在东海的两条平行线上排成一列,这是自去年 12 月以来的第三次协调集结,每艘渔船都向东更远,距离日本更近。同一天,五角大楼证实,的黎波里号航空母舰(之前驻扎在太平洋的第 31 海军陆战队远征部队)上的 2,500 名美国海军陆战队员正在重新部署到中东。

太平洋舰队正在精简。平壤正在测试这一空缺。北京的海上民兵正在绘制地图。

这一切都与朝鲜无关。这些都与渔船无关。所有这一切都可以追溯到一条水道——宽 33 公里,关闭了 14 天——以及关闭所引发的一系列后果。

霍尔木兹海峡不仅仅是一个石油咽喉要道。它是美国全球安全架构的承重墙。除去它,压力就不会留在中东。它通过能源市场、通过联盟承诺、通过为从首尔到台北到塔林的每项美国安全保证提供保障的军事力量态势进行传播。日本海中的导弹和冲绳附近的渔船是这种传播的第一个可观察到的证据。

问题不在于油价是否保持在 100 美元以上——几乎肯定会走高,机构预测范围从 95 美元(EIA,如果霍尔木兹在几周内重新开放)到巴克莱尾部情景中的 120-150 美元,伯恩斯坦的需求破坏门槛为 155 美元。真正的问题是,在能源短缺、安全真空和外交分裂的多重压力下,哪些国家、哪些联盟和哪些政治体系首先崩溃,以及谁能够填补这一空白。

这就是那张地图。

我。十四天:72 美元前往深渊

这个时间表值得仔细阅读,因为每一集都遵循相同的模式:政策信号压缩价格飙升,物理现实在 48 小时内重新确立。

第 1-4 天(2 月 28 日 - 3 月 3 日)。美国和以色列军队袭击伊朗。布伦特原油价格从约 72 美元跃升至 85 美元,四天内上涨 18%。伊朗立即进行报复:对美国在海湾的军事基地、沙特阿拉伯的 Ras Tanura 炼油厂(产能:55 万桶/天)以及卡塔尔的液化天然气出口设施进行导弹和无人机袭击。欧洲天然气价格两日上涨48%。每天大约有 20% 的全球石油和液化天然气通过霍尔木兹海峡运输,该海峡实际上已关闭。

第 5-7 天(3 月 4-6 日)。特朗普宣布美国海军为海湾航运提供护航和贸易保险担保。市场短暂地松了口气。随后中央司令部确认已摧毁 16 艘伊朗布雷船——这意味着水雷已经埋在水中。超过 200 艘船只报告霍尔木兹附近 GPS 信号异常。 “解除警报”并非解除警报。

第 8 至 10 天(3 月 7 日至 9 日)。 沙特阿拉伯、阿联酋、科威特和伊拉克被迫削减产量(总计约 6.7 mb/d),因为海峡是它们唯一有意义的出口路线,而存储量已接近极限。布伦特原油盘中交易价格为 119.50 美元。这比战前收盘价 72 美元上涨了 66%。

第 10-11 天(3 月 10 日)。特朗普告诉福克斯新闻,冲突将“很快”结束,并暗示可能会豁免对石油和天然气的制裁。 WTI 跌幅超过 10%,一度跌破 80 美元。同一天,五角大楼将 3 月 10 日描述为“冲突开始以来打击最激烈的一天”。政策信号和实际现实指向相反的方向。两者都不可能是真的。市场在接下来的 48 小时内寻找答案。

第 12-14 天(3 月 11-13 日)。 IEA 宣布其历史上最大规模的协调战略储备释放:4 亿桶。 WTI 短暂上涨,然后下跌,然后在数小时内再次攀升。 3月12日,两艘油轮在伊拉克海域遭遇袭击。阿曼紧急清理米纳法哈尔出口码头。截至 3 月 13 日收盘,布伦特原油价格接近 101 美元。 WTI 价格为 99.30 美元。

第 14 天(3 月 13 日至 14 日)。 24 小时内发生了四项事态发展,改变了冲突的轨迹。首先,特朗普宣布美军“摧毁”了伊朗哈格岛上的军事目标——该码头处理着伊朗约 90% 的石油出口——并警告称,该岛的石油基础设施可能是下一个目标。几小时后,五角大楼确认部署第 31 海军陆战队远征部队和“的黎波里”号两栖攻击舰,以及大约 2,500 名海军陆战队员,从日本前往中东。海军陆战队远征部队是专门为两栖登陆和确保海上咽喉要道而建造的。 NBC新闻援引一位美国官员的话说,中央司令部之所以要求派遣部队,是因为“这场战争计划的一部分是让海军陆战队提供使用选择”。的黎波里号是在吕宋海峡附近被商业卫星发现的,距离伊朗附近海域大约有 7 到 10 天的时间。然后,3 月 14 日,朝鲜向日本海发射了大约 10 枚弹道导弹,这是 2026 年最大的单次齐射。同一天,法新社报道称,在东海发现了 1,200 艘中国渔船,形成了第三个协同编队,该编队比 12 月和 1 月的事件更靠东,更靠近日本水域。

这是两个轴上的质的转变。在 13 天的时间里,美国只进行了空袭行动,而霍尔木兹海峡仍然处于关闭状态。远征部队的部署表明,华盛顿正准备对海峡进行实体争夺——而不仅仅是在海峡周围进行轰炸。国防部长赫格斯明确表示了这一意图:“我们不会允许这个海峡继续存在争议。”但远征部队是太平洋地区唯一一支前沿部署的快速反应部队,在其出发后数小时内,平壤和北京的海上民兵就开始测试这一空缺。霍尔木兹危机不再局限于海湾地区。

14 天的模式是明确的:每项政策响应都需要 24 到 48 小时。每次宣布后的几个小时内,物理现实就会重新显现出来。现在,其后果正在从能源市场蔓延到霍尔木兹所承保的全球安全架构中。但从第 14 天开始,问题已经扩大:危机不再仅仅与供应数学有关。问题在于美国能否在其盟友的储备耗尽之前实际重新开放海峡,以及这一尝试将付出什么代价。

II. SPR 错觉

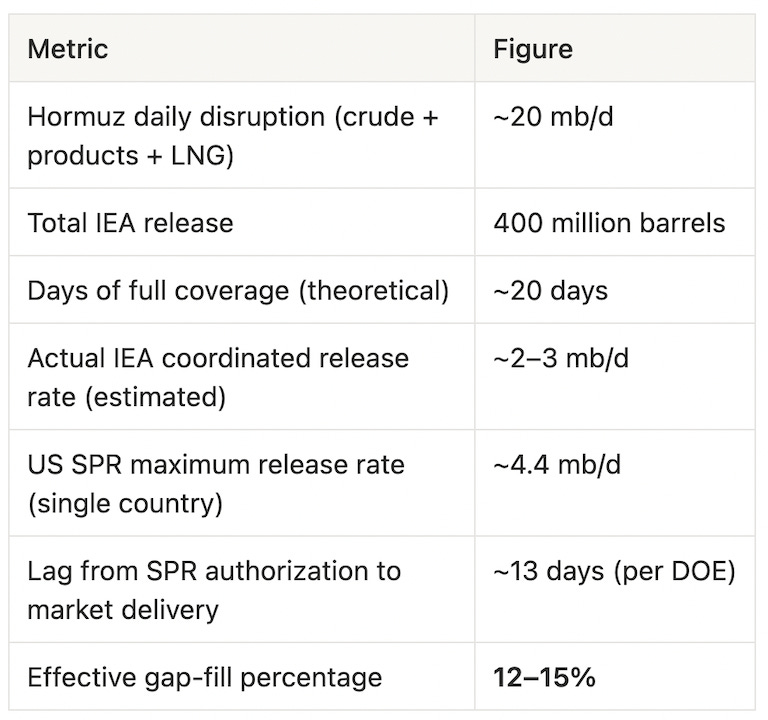

IEA 释放 4 亿桶石油是该机构 52 年历史上第六次协调储备削减,也是规模最大的一次。它是 2022 年俄罗斯入侵乌克兰后释放的 1.82 亿桶石油的两倍多。据美国能源部称,仅美国就承诺释放 1.72 亿桶石油,约占总量的 43%,预计从下周开始交付,预计需要 120 天的缩减期。

听起来很果断。数学不是。

填补缺口的数字才是最重要的。根据路透社关于释放机制的报道,按照现实的协调释放速度(不是总体桶数,而是实际每日流量),IEA 的历史性干预覆盖了 12% 至 15% 的供应中断。它无法填补其余部分。除了重新开放海峡之外没有什么办法。

黑金投资者创始人、霍尔木兹力学最准确的分析师之一加里·罗斯 (Gary Ross) 坦白地说:

<块引用>“除非冲突结束,否则如果不破坏需求和提高价格,这种情况就无法控制。”

市场同意了。 WTI 因 IEA 公告而大幅下跌,随后于当天回升。正如 NBC 新闻指出的那样,协调发布“未能降低价格”。这个信号是政治性的。不足是身体上的。

进一步的结构性限制:SPR的释放缓解了液态原油库存的压力,但不涉及液化天然气。日本和韩国最严重的脆弱性(详见下文)不是石油。它是液化天然气,不存在可与IEA石油机制相媲美的战略储备体系。

III.沙特管道神话

沙特阿拉伯是唯一拥有理论上绕行路线的主要海湾产油国:东西方管道,从东部油田延伸至红海延布港,铭牌产能为 7 mb/d。沙特阿美首席执行官阿明·纳赛尔证实,该管道正在努力实现最大利用率。据报道,有 27 艘 VLCC 正在前往延布的途中。港口装载量已飙升至创纪录的 2.72 mb/d。

这个数字 — 2.72 mb/d — 是真实数字。不是 7 mb/天。

铭牌与实际之间的差距反映了 Argus Media 分析师列出的几个硬性限制:

延布码头的设计无法处理 7 mb/d 的装载流量。泊位容量和泵送基础设施的物理上限远低于管道的理论吞吐量。该管道本身有双重目的——出口合同和为沙特阿美西部炼油厂供应原料——这意味着同样的产能存在内部竞争。在胡塞武装威胁下,红海保险保费增加了一倍多,进一步压缩了有效绕行。

Per Argus Media:“管道限制和有限的装载能力意味着该路线只能部分抵消损失。”

净有效旁路容量:大约 2.5 至 3 mb/d。在约 20 mb/d 的中断情况下,沙特管道弥补了大约 15% 的缺口。如果加上 12-15% 的 IEA SPR,目前正在运行的任何机制都无法解决超过三分之二的供应缺口。

理论上现在存在第三条途径:美国海军护航迫使该海峡部分重新开放。财政部长贝森特于 3 月 12 日确认了该计划,表示海军将“在军事上尽快”开始护航油轮。但能源部长克里斯·赖特当天更加坦诚:“我们根本就没有准备好。我们现在所有的军事资产都集中在摧毁伊朗的进攻能力。”赖特估计护航行动可能会在月底开始——《华尔街日报》援引两名美国官员的话称,时间表将在一个月或更长时间。限制因素不是船舶;而是船舶。而是水雷已经在水中,美国在该地区没有部署成熟的水雷反制部队。在沿海反舰导弹连被消灭和水雷被清除之前,护航只是愿望,而不是后勤。

四。谁先打破

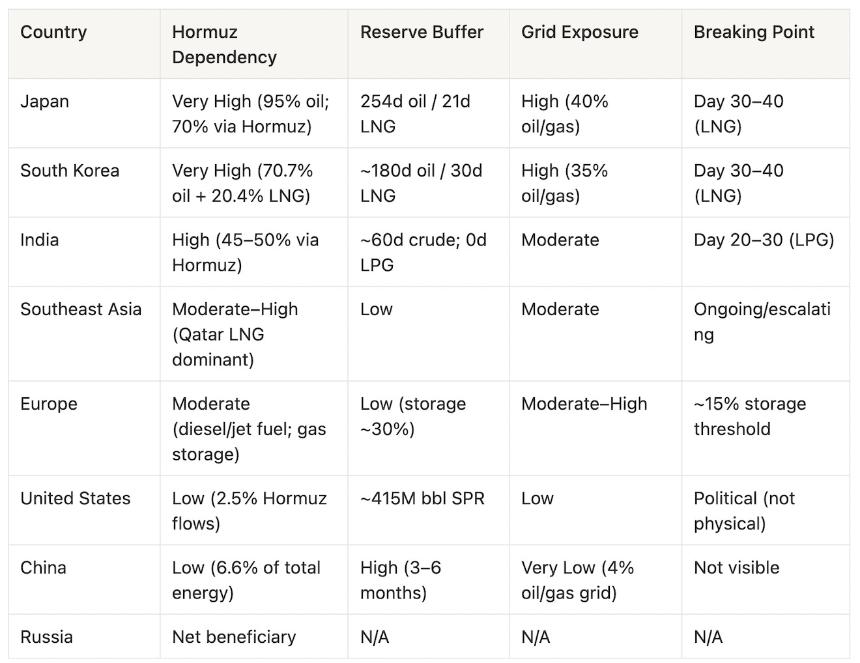

供应冲击是全球性的。断点不是同时发生的。每个国家的时钟都以不同的速度滴答作响,这取决于其进口依赖度、储备深度、电网构成以及社会对价格痛苦的容忍度。从第 14 天开始,一个新的时钟与其他时钟一起运行:美国军方实际重新开放海峡的时间表,估计是从现在起 2 至 4 周后。 “谁先突破”的问题现在是储备耗尽、外交解决和军事干预之间的三方竞赛。以下是按国家/地区从最易受影响到最少的漏洞排名。

日本

日本是地球上受霍尔木兹海峡关闭影响最大的结构性主要经济体。大约95%的石油来自中东,其中大约70%直接通过海峡。日本的石油战略石油储备——名义上的供应量为 254 天——为原油提供了重要的缓冲。但日本的液化天然气立场是致命一击:该国仅持有约三周的液化天然气库存,而液化天然气为日本电网的大约 40% 提供燃料。

福岛事件的讽刺在这里是苦涩的。 2011 年灾难迫使日本关闭其核舰队后,卡塔尔的液化天然气供应成为日本家庭照明的生命线。现在,这条生命线已被切断——卡塔尔的液化天然气出口设施是伊朗第一天报复性袭击的目标之一。牛津能源公司分析师指出,如果供应中断持续下去,液化天然气现货价格可能会飙升 170%。

日本已经采取单方面行动。它宣布于3月11日从国家储备中释放8000万桶——15天的消费量。四十二艘日本运营的船只仍被困在海峡内或附近。自冲突开始以来,日经指数已下跌约 7%;在避险策略被打乱的世界里,日元作为避险货币的地位正在走弱。

实物短缺风险:第 30-40 天(液化天然气电网耗尽阈值)。

韩国

韩国的风险敞口在结构上与日本几乎相同,但政治熔断机制已经触发。该国 70.7% 的石油和 20.4% 的液化天然气来自中东。石油和天然气合计约占电网发电量的 35%。

韩国综合股价指数 (KOSPI) 下跌超过 12%,在该指数最糟糕的日子里触发了交易暂停。韩国总统李在明呼吁设定燃油价格上限,这是自亚洲金融危机以来的首次,总统政策负责人表示,据报道正在讨论将上限定为每升 1,900 韩元。炼油厂将进口量削减 30%。小型独立加油站已开始关闭。

西方投资者一直低估的下游后果:三星和SK海力士半导体工厂需要稳定、不间断的电力。如果电网变得不稳定——不是因为停电,而是因为滚动电压管理——晶圆厂产量就会下降,生产计划也会推迟。这不是韩国的问题。这是一个全球人工智能基础设施问题,存在于数据中心资本支出假设中。

现代研究公司估计,100 美元的石油价格意味着韩国 GDP 会受到 0.3 个百分点的拖累,CPI 会加速 1.1 个百分点,经常账户恶化约 260 亿美元。

实物短缺风险:第 30-40 天(与日本液化天然气耗尽同步)。

印度

印度每天消耗大约 5.5 mb。其中大约 45-50% 流经霍尔木兹。政府获得了华盛顿的 30 天豁免,允许继续购买俄罗斯石油——这对原油来说是一个有意义的缓冲。但液化石油气的情况没有类似的解决方法。

印度约 62% 的液化石油气是进口的,其中约 90% 是通过霍尔木兹海峡运输的。印度没有战略液化石油气储备。在印度,液化石油气并不是优质燃料,而是数亿家庭的基本烹饪燃料。大约 80% 的印度餐厅使用液化石油气作为主要热源。由于原料流枯竭,门格洛尔炼油厂已被迫暂时关闭。

社交传播已经显而易见。在浦那,由于液化石油气供应紧张,火葬场已从天然气火葬场转向木材和电力设备。这不是一个抽象概念。这对数千万人的日常生活造成了干扰。

据路透社援引印度政府消息人士的话称,伊朗已同意允许悬挂印度国旗的油轮通过该海峡——这是一项双边安排,可以在液化石油气供应链仍然中断的情况下提供部分原油缓解。三菱日联金融集团的经济学家指出了滞胀动态:卢比贬值,消费者物价指数加速,油价每上涨 20 美元/桶,企业收益将减少约 4 个百分点。社会层面的冲击风险:第 20-30 天(液化石油气供应链压力达到临界家庭渗透率)。

东南亚

该地区的脆弱性是分散的,但正在加剧。巴基斯坦大约 99% 的液化天然气来自卡塔尔,汽油价格在两周内上涨了 20%。菲律宾缩短了工作周;印度尼西亚实行旅行限制;孟加拉国削减了斋月照明。财政空间有限的经济体已经开始实行配给。

压力阈值:活跃且加速。

欧洲

欧洲对霍尔木兹的影响不那么直接——该大陆约 30% 的柴油和 50% 的喷气燃料来自海湾——但天然气规模却很严重。欧洲天然气存储以约 30% 的比例陷入冲突,在 2021-2024 年缩减周期后已经处于历史低位。至关重要的是,荷兰在冲突爆发时的存储量仅为 10.7%。自2月28日以来,天然气价格已上涨75%。燃气发电量环比下降33%。

俄罗斯是影子受益者。自冲突开始以来,俄罗斯化石燃料出口收入增加了约 60 亿欧元,其中估计额外增加了 6.72 亿欧元的溢价。欧洲各国政府面临的战略悖论:特朗普可能会提出放松对俄罗斯的制裁,以此作为淹没欧洲天然气市场和降低能源价格的机制——这将同时破坏欧洲大陆花了四年时间建立的欧洲安全政治架构。这不是一个假设。这是华盛顿流传的一个积极的政策选择。

危机阈值:当天然气储存量达到约 15% 时,按照目前的燃烧速度,在库存量最低的市场中,这需要几周的时间。

美国

在本次分析中,美国经济是孤立性最强的主要经济体,也是政治暴露程度最高的经济体。

身体暴露是真实的但适度的。霍尔木兹吞吐量中只有大约 2.5% 运往美国。 SPR 储量约为 4.15 亿桶——以 1990 年后的标准衡量,处于历史低位,但足以支撑国内市场几个月。页岩产能可以做出反应,但从钻探决策到增量产量有 3 至 6 个月的滞后期。美国的生产没有短期修复。

加利福尼亚州的例外情况很重要:加利福尼亚州 61% 的炼油厂原油输入是进口的,其中约 30% 是通过霍尔木兹海峡运输的。加州的汽油价格与全国平均水平相比已经处于异常水平,而且该州缺乏备用炼油厂产能来大规模替代国内原油。

美国真正的脆弱性是政治上的,而不是物质上的。汽油价格是美国选民最清晰的经济信号。特朗普同时对伊朗发起军事行动,并公开承诺降低油价——在霍尔木兹海峡仍处于关闭状态、海湾阿拉伯国家每天六吨以上的石油产量仍处于停产状态的情况下,这一承诺实际上是不可能兑现的。矛盾不可能无限期地持续下去。有些东西出现了问题:要么是军事行动的政治支持,要么是政府在经济管理方面的可信度,或者两者兼而有之。

政治传播风险:活跃。实物短缺风险:短期内较低,如果冲突持续超过 90 天且战略储备金缩减会压缩缓冲,则会上升。

中国

中国是结构性异常——这也是本文以此结尾的原因。

霍尔木兹过境石油约占中国一次能源消费总量的6.6%。中国的战略石油储备估计为1.2至14亿桶,相当于大约3至6个月的进口量。目前新能源汽车占中国新车销量的50%以上;电网对石油和天然气的依赖度约为4%。自冲突开始以来,沪深 300 指数下跌 0.1%。人民币的表现优于所有主要亚洲货币。

中国已停止成品油出口,以保护国内供应,而其他国家则在争夺替代品。根据 CNBC 对卫星船只数据的跟踪,伊朗原油继续通过海峡流入中国(根据 TankTrackers,自 2 月 28 日以来至少有 1170 万桶)。伊朗对其自身封锁的遵守似乎是有选择性的。

中国不是旁观者。这是支点。

俄罗斯

俄罗斯是唯一明确的受益者。两周内化石燃料出口收入增量约为 60 亿欧元。原本不再依赖俄罗斯供应的欧洲和亚洲买家现在正在紧急寻找替代品,而俄罗斯管道和北极液化天然气航线突然成为地缘政治上最简单的选择。华盛顿对印度购买俄罗斯石油的豁免实际上重新打开了最初制裁制度部分关闭的销售窗口。用一位市场参与者的话说,对俄罗斯能源的需求“显着增加”。

V.漏洞矩阵

VI。需求破坏:自我熄灭机制

石油总是有它自己的治疗方法。如果价格足够高,需求就会崩溃,危机无需外交手段就能解决。问题是什么价格足够高——在这个周期中,答案比大多数人想象的要高。

Bernstein 分析师 Irene Himona 在这方面做了最仔细的研究:以今天的美元计算,要达到实质性抵消霍尔木兹供应损失所需规模的需求破坏,大约需要2026 年全年平均价格为 155 美元/桶,即“石油负担”(石油支出占全球 GDP 的比例)达到 2007 年观察到的 5.2% 水平的阈值,历史上与有意义的消费减少相关。低于这一水平,世界基本上会继续购买,并通过通货膨胀、增长拖累和财政转移支付来吸收痛苦。

机构对解决方案(霍尔木兹逐渐重新开放)的预测如下:EIA 预计布伦特原油价格将在两个月内保持在 95 美元以上,然后在第三季度跌至 80 美元;根据 Daan Struyven 的最新报告,高盛将 2026 年第四季度布伦特原油和 WTI 目标分别修订为 71 美元和 67 美元。如果冲突再持续两周,巴克莱将 120 美元标记为可测试,尾部情景为 150 美元。

关键的见解是需求破坏并不均匀。

汽油——约占全球需求的 25%——是有弹性的。司机可以自行减少行驶里程。柴油(17%)和喷气燃料(8%)的底线更硬:货运运行是因为供应链需要,航班运行是因为商务旅行没有替代品。石化产品(15-17%)是纯粹的投入成本通胀。液化石油气和取暖燃料是不对称最严重的领域。在发展中国家,当液化石油气增加一倍时,反应不是“少开车”,而是“更换燃料、减少营养、减少活动”。贫穷国家不会逐渐摧毁需求。他们打破了。

VII.持续时间碎片:异步问题

当前大多数评论中的主要分析错误是将其视为单一同步的全球冲击。它不是。这种冲击因国家、产品类型和储备深度而不同,而且最重要的是,突破点出现的时间不同。

日本和韩国在海峡持续关闭的大约第 30-40 天达到实际短缺阈值,届时液化天然气库存耗尽,现货采购要么不可能,要么在经济上不合格。印度的液化石油气供应链已经面临巨大压力;大约第 20-30 天,社会层面的混乱变得难以遏制。当天然气储存达到 15% 的水平时,欧洲的危机就会到来——这是当前燃烧率和俄罗斯供应灵活性缺乏的函数;在暴露程度最高的市场,这只需几周的时间。美国对能源的政治压力在第 60-90 天不断升级,因为 SPR 的缩减明显压缩了储备缓冲,而油价上涨成为持续的选举负担。

这些不同的时钟产生了深刻的协调问题。停火谈判需要各方同时寻求解决方案。日本和韩国可能会在第 35 天尖叫起来;华盛顿可能仍在政治上消化这场危机;印度可能已经发生过街头液化石油气骚乱。在看着俄罗斯出口收入激增的同时,欧洲也面临着自己的算计。

异步性是伊朗的战略资产。盟军的统一反应需要在相同的时间感受到相同的压力。那不会发生。

这也是为什么释放 SPR(物理上不充分)在政治上是必要的。它买的不是石油,而是时间:调整时间,集体行动的出现,阻止日本、韩国和印度在华盛顿准备好参与之前与德黑兰达成双边安排。

所购买的时间是否得到有效利用取决于两件事:本周末巴黎会发生什么,以及美国军方能否争分夺秒。

八。三个剧院

上述石油分析假设存在一场危机。截至第 14 天,共有 3 个。

太平洋并不安静

远征部队的离开造成了威慑真空,数小时内就受到了调查。第 14 天事件的细节——哈格岛、的黎波里重新部署、朝鲜齐射、捕鱼船队编队——都在第一节中进行了分类。这里重要的是它们背后的模式。

中国海上民兵编队并非临时拼凑而成。地理空间公司 ingeniSPACE 跟踪的 AIS 数据显示,自 2025 年 12 月以来发生了三起协调一致的事件,每一次都更大、更东:12 月,2,000 艘船只排成两个平行的倒 L 形,每个长 400 公里; 1 月份,在 320 公里长的矩形区域内,有 1,400 人;本周为 1,200,接近日中中线。数百艘船只参加了多项活动,几乎全部来自浙江省——几个著名的民兵港口的所在地。 CSIS 的格雷戈里·波林 (Gregory Poling):“几乎可以肯定他们不是在捕鱼,我想不出任何非国家主导的解释。”五角大楼自己的中国军事评估证实,北京资助这些部队“执行官方任务”,并且它们可以通过为外国军事干预设置障碍来支持作战行动。

朝鲜的齐射是 2026 年最大的一次齐射,是在美韩自由之盾演习期间降落的,随着美国资产向海湾地区转移,演习的节奏正在放缓。平壤外交部已经将这场战争描述为“强者可以在任何条件下生存和发展;弱者将成为制裁和侵略的受害者”的证据。

这两个事件单独来看都不是史无前例的。排序是。日本正在吸收液化天然气耗尽时钟、中国民兵船只在其西南方向、朝鲜导弹在其西部——而其安全保障则在相反的方向上航行。台湾正在观看自己封锁的预演。伊朗战争在太平洋打开了一扇窗,一直在做准备的行动者正在实时检验它。

霍尔木兹困境

远征部队的重新部署并不是任意的。华盛顿有真正的行动需求:两周的空袭摧毁了 15,000 多个目标,并使伊朗海军“战斗无效”,参谋长联席会议主席丹·凯恩将军表示。但空中力量尚未重新开放霍尔木兹。水雷都在水里。沿海反舰导弹连尚未完全失效。海峡仍然关闭。 MEU 增加了空中力量无法做到的功能:将靴子放在地面上的选项。

迫使霍尔木兹开放的三种操作方案是合理的。首先,护航优先:美国削弱伊朗海岸防御、扫雷,并在三月下旬开始护航商业油轮。能源部长赖特估计这可能会在月底开始; 《华尔街日报》援引官员的话说,需要一个月或更长时间。其次,哈格岛的夺取:远征军袭击了处理伊朗90%石油出口的码头——特朗普已经袭击了那里的军事目标,并威胁到了石油基础设施。第三,沿海清理:沿指挥海峡的150公里伊朗海岸线开展行动。澳大利亚战略政策研究所将此比作“加里波利乘以十”。伊朗革命卫队在海峡地区拥有 20,000 名海军部队,并花了四十年的时间演练如何击退此类袭击。

时间线非常短。的黎波里距阿拉伯海 7 至 10 天。如果它在第 22-25 天左右到达,军事选项就会在日本和韩国的液化天然气储备接近临界水平时开始运作。在第 25 天左右开始的成功护航行动可以在暴露程度最高的盟友遭遇物资短缺之前开始对其进行救援。一次失败的行动——一艘油轮在护航下被击中,一场两栖攻击陷入困境——将会加速危机。

即使成功也有上限。 “在武装护卫下开放”的海峡与开放的海峡不同。 Lloyd’s List estimates a basic escort operation would require 8 to 10 destroyers protecting 5 to 10 vessels at a time — a fraction of the pre-war traffic of nearly 100 transits per day. Forced reopening delivers a trickle, not a flood.

The Two-Front Bind

This is the strategic trap that no section of this article can analyze in isolation. The US needs the MEU in the Gulf to reopen Hormuz before its allies’ reserves run dry. But the MEU’s departure from the Pacific has created a deterrence vacuum that is being probed within hours. Every day the Tripoli steams west is a day the Pacific grows more permissive for actors who have been waiting for exactly this kind of American overextension.

The US military is not short of total capacity. It is short of capacity in two oceans at once. And the Iran war — which began as an air campaign that was supposed to end “very soon” — is now forcing a resource allocation decision between the Middle East and the Indo-Pacific that American defense strategy has spent two decades trying to avoid.

The oil crisis described in Sections I through VII is the trigger. What is emerging in Section VIII is the consequence: a global security architecture being tested at multiple stress points simultaneously, with the same finite set of assets being asked to hold every line.

IX. The Paris Prelude — Under Three Shadows

Tomorrow, US Treasury Secretary Scott Bessent sits down with Chinese Vice Premier He Lifeng in Paris. According to the Associated Press and Reuters, the meeting runs Sunday and Monday — a preparatory session for President Trump’s scheduled state visit to Beijing beginning March 31, his first to China since 2017. On the American side, the public agenda is trade: reducing Chinese purchases of Russian and Iranian oil, increasing Chinese imports of US soybeans, Boeing aircraft, and energy.

The agenda was overtaken by events before the plane landed.

Bessent is not walking into a trade negotiation. He is walking into a room where the man across the table holds leverage over all three theaters described above — the Gulf, the East China Sea, the Korean Peninsula — and knows it. Beijing did not create any of these crises. But Beijing is the only actor positioned to resolve or exploit all three simultaneously. That is the hand He Lifeng brings to Paris.

Hours before the meeting was announced, CNN reported that Iran is considering allowing a limited number of oil tankers to pass through the Strait of Hormuz — on one condition: oil cargo must be settled in Chinese yuan, not US dollars. A senior Iranian official confirmed the framework to CNN. RBC-Ukraine, citing the same reporting, framed it precisely: tankers can pass, but only if trade is denominated outside the dollar system.

Iran is not simply offering a passage fee. It is offering China the prototype of a new monetary architecture: yuan-denominated energy settlement enforced at the world’s most critical chokepoint. If China accepts — and if tankers begin flowing on yuan terms — Beijing will have embedded its currency in the infrastructure of global energy trade in a way that no financial engineering or diplomatic agreement could have achieved in peacetime.

The ask Bessent carries into the room — “pressure Iran, buy less Russian oil, buy more American stuff” — was already a difficult pitch. It is now almost absurd. The US is asking China to forgo a once-in-a-generation monetary upgrade, restrain its maritime militia at the moment of maximum American overextension, and help stabilize a Korean Peninsula it has no interest in stabilizing — in exchange for soybean purchases and goodwill toward a state visit.

Bessent is not arriving empty-handed. He is arriving with that MEU steaming toward the Gulf. The implicit message: if China does not broker a resolution, the US will attempt to force one, and the resulting escalation would be far messier for everyone — including for China’s own energy flows and for the yuan-settlement architecture that Iran is offering. A negotiated reopening preserves Beijing’s leverage. A military reopening destroys the conditions under which that leverage operates.

But the MEU is also Bessent’s weakness. Beijing knows that every day the Tripoli steams west is a day the Pacific grows more permissive. The military card that gives Washington leverage on Hormuz simultaneously gives Beijing leverage on everything else. China does not need to escalate in the Pacific. It just needs to keep rehearsing, keep probing, keep demonstrating that the US cannot hold two oceans at once — and let the implications do the negotiating.

China’s leverage at the table is not static. It compounds daily. Every day Japan and Korea inch toward their LNG exhaustion threshold, Washington’s ask becomes more urgent and its concession space expands. Every day the Pacific deterrence gap widens, the price of Chinese restraint rises. The asynchrony of breaking points described in Section VII does not operate symmetrically — it operates in Beijing’s favor across every theater.

<块引用>“The only broker in the room is Beijing. The price will be high.”

What can Washington offer that might compete? Sanctions relief on Chinese tech exports, a CHIPS Act rollback, movement on Taiwan — these are not trade-desk concessions. They are strategic architecture decisions that require principals-level authorization, not Bessent in Paris. Which is precisely the point: this meeting is Washington taking the measure of China’s price before Trump arrives in Beijing on March 31.

Carnegie Endowment analysts have long argued that Beijing’s energy diplomacy operates on a horizon Washington’s electoral cycle cannot match. Iran’s yuan offer is not a surprise to Beijing. It has been discussed in bilateral channels for years. The Hormuz crisis moved it from theoretical to operational. The Pacific vacuum moved it from operational to urgent.

Four scenarios are now live. In the first, China brokers a face-saving Hormuz reopening, restrains the militia activity, and yuan settlement remains marginal — the EIA’s $70-range year-end Brent baseline assumes this. In the second, China extracts full structural concessions on Taiwan, tech, and currency architecture; Hormuz reopens on Chinese terms; the Pacific probing continues because Washington has conceded the leverage that would have stopped it. In the third, diplomacy stalls and the US forces the Strait open militarily around Day 25–30 — but the Pacific remains exposed, and the “victory” in the Gulf is purchased at the cost of deterrence in the theater that actually matters for the next 30 years. In the fourth, both tracks fail — diplomacy produces nothing, the military operation is delayed or bloodied — and Japan, Korea, and India enter physical rationing while the Pacific tests move from rehearsal to execution.

The Paris meeting will not resolve any of these crises. But it may be the last moment at which they are still separate crises — before they merge into a single, cascading confrontation that no one in the room has the authority to stop.

What Is Actually Breaking

This article began as an energy analysis. It is now a war assessment.

Two-thirds of the global oil shortfall has no solution in operation or in transit. And on Day 14, the crisis stopped being about energy: the US pulled its only forward-deployed Marine force out of the Pacific, and within hours both Beijing and Pyongyang moved to test the vacancy — not in response to the redeployment, but alongside it, as if the script had already been written and the cue had just arrived.

The question this article set out to answer — who breaks first under $100 oil — now sits inside a larger and more dangerous one: how many fronts can open before the system that is supposed to hold them closed admits it cannot hold them all?

This is not an abstract structural question. It is a concrete operational one with a near-term timeline.

The MEU arrives in the Gulf around Day 22–25. If the Strait is forced open by Day 30, Japan and Korea survive their LNG clocks — barely. But the Pacific remains exposed for every day of that operation and for weeks afterward. If the Strait is not forced open, allies begin rationing and the diplomatic leverage shifts decisively to Beijing. If the Pacific probing escalates while the MEU is in the Gulf — a fishing fleet incident near the Senkakus, a North Korean test that overshoots, a Chinese naval exercise that crosses a line — the US faces a choice it has spent 80 years of alliance architecture trying to avoid: which theater to abandon.

Tomorrow in Paris, Bessent and He Lifeng sit across from each other with all of this on the table. The American offer is trade concessions and the implicit threat of military escalation. The Chinese counter is restraint — in the Gulf, in the East China Sea, on the Korean Peninsula — priced at whatever Beijing decides restraint is worth this week. Next week it will cost more.

The next 48 hours are not a negotiation window. They are the last interval before the crises in the Gulf, the East China Sea, and the Korean Peninsula stop being parallel and start being the same war.

“Who breaks first” is no longer about oil. It is about whether anyone in the room has the authority — and the nerve — to stop what is coming.

Invalidation Signals

The bearish thesis (oil prices sustained above $100, structural fragility deepening) requires monitoring against these exit conditions:

-

Rapid Hormuz reopening: A ceasefire or Iranian decision to reopen the Strait within the next 10–14 days would collapse the geopolitical premium and validate the EIA/Goldman Q3–Q4 $70–$80 range. Watch for: official Iranian announcement accompanied by independent maritime confirmation of vessel movement.

-

Saudi pipeline fully operationalized: If Yanbu loading consistently exceeds 3.5 mb/d for more than a week, the theoretical 7 mb/d capacity is being approached in practice. This would be a material supply-side relief signal.

-

IEA release rate beats estimates: If daily SPR flows from IEA members track at 4+ mb/d sustained, the effective gap-fill rises above 20% — still insufficient, but meaningfully better than base case.

-

Demand destruction arrives early: If global air travel data (IATA weekly) and US diesel consumption (EIA weekly) show simultaneous sharp declines, the $120–$155 demand-destruction mechanism may be triggering ahead of schedule. This resolves oil prices but creates a new problem: recession pricing in growth assets.

-

US escort operations begin successfully: If the Navy begins escorting tankers through Hormuz before Day 30 without a major incident (no escorted vessel struck, no mine detonation in convoy), the military path becomes the primary resolution mechanism. Watch for: CENTCOM announcement of escort corridor, confirmed commercial vessel transits under protection, and insurance markets beginning to write new policies for escorted passage. Even partial success — 10 to 15 escorted transits per day — would meaningfully change the supply math.

-

China successfully embeds yuan settlement into Strait passage mechanism: This is not a short-term oil price signal. It is a long-duration structural shift in the petrodollar architecture. Watch for: Iranian government announcement of yuan settlement requirements for passage, followed by observable vessel traffic resuming with Chinese financial intermediaries. If this materializes, it is the most consequential development in the global monetary order since the 1973 oil embargo — and it will not initially look like a crisis. It will look like a solution.

-

Pacific escalation crosses from rehearsal to incident: The thesis that Beijing and Pyongyang are probing, not attacking, requires that the probing remain below the threshold of a kinetic or territorial event. Watch for: any physical confrontation between Chinese maritime militia and Japanese Coast Guard near the Senkakus; a North Korean missile that lands inside Japan’s exclusive economic zone closer to shore than previous tests; a Chinese naval exercise that transits the Taiwan Strait or enters Japanese territorial waters while the 31st MEU is in the Gulf. Any of these would transform the multi-theater pressure from a leverage play into a genuine second-front crisis, radically compressing the timeline for every other variable in this analysis.

This is the second installment in Garrett’s Signal’s Hormuz series. The first piece — Home Is the Battlefield — mapped the domestic shock: how the Strait closure translates into household-level pain across economies dependent on Gulf energy. This piece follows the fractures outward — from homes to hemispheres — tracking where the crisis has spilled beyond energy markets into the global security architecture, alliance commitments, and the multi-theater confrontation now taking shape across the Gulf, the East China Sea, and the Korean Peninsula.

Garrett’s Signal · March 2026 · Day 14 of the conflict